The Pros and Cons of Annuities

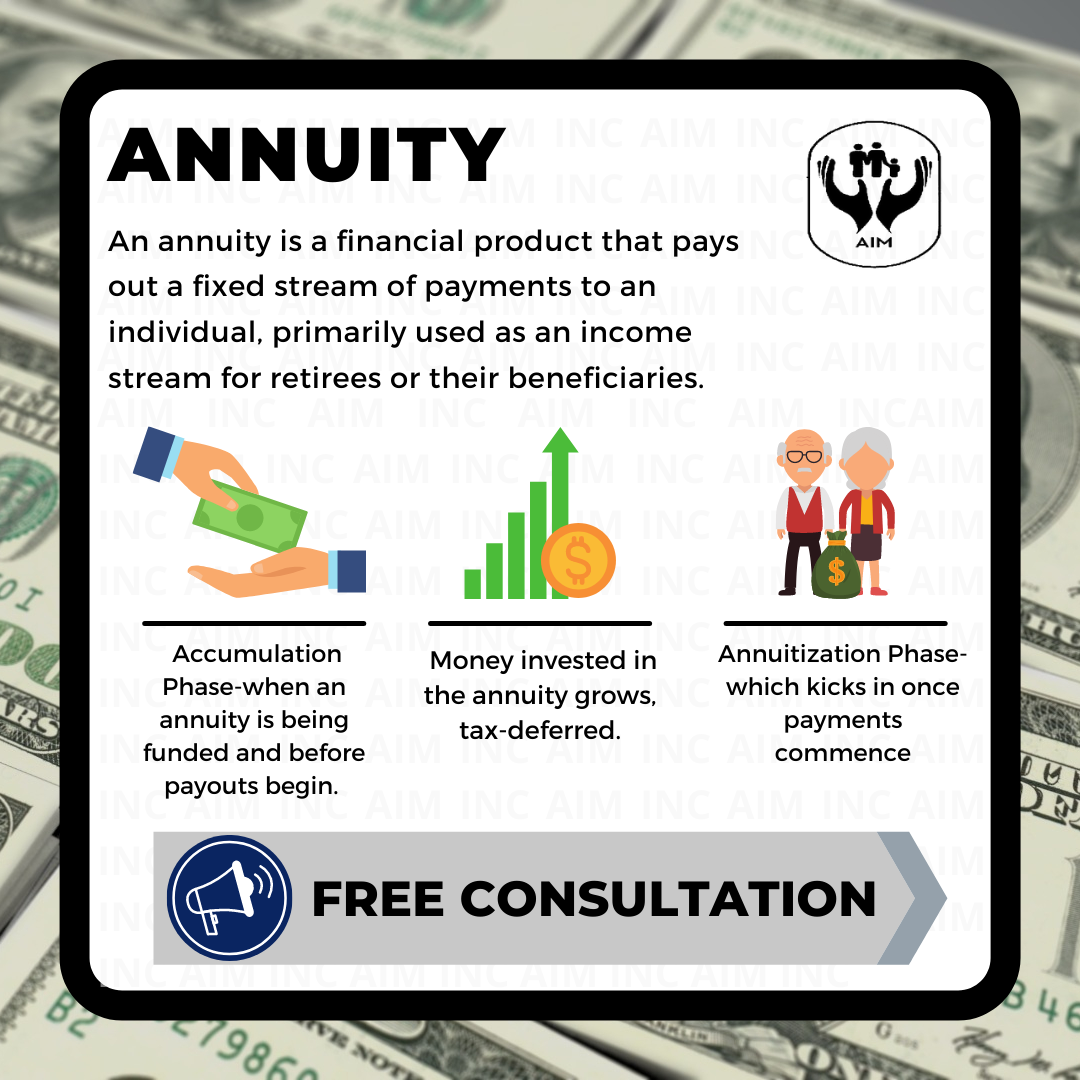

An annuity is an insurance product that can be used as part of a retirement strategy. Annuities are a popular choice for individuals who want to receive a steady income stream in retirement. An annuity works by depositing an investment in the annuity, the insurance company will invest your money to generate income and deposit back into your account. Due to your money being invested, the account is locked against any withdrawals for an amount of time until the account matures.

Once the annuity has matured, payments can be set up on a future date or series of dates while paying taxes on it. The size of your payments are determined by a variety of factors, including the length of your payment period. How much you receive depends on whether you opt for a guaranteed payout (fixed annuity) or a payout stream determined by the performance of your annuity's underlying investments (variable annuity). While annuities can be useful retirement planning tools, they may not fit your investment needs if the premiums are not within your budget. An annuity should be researched thoroughly first, before deciding whether it's an appropriate investment for someone in their situation.

There are two basic types of annuities: deferred and immediate. With a deferred annuity, your money is invested for a period of time until you are ready to begin taking withdrawals, typically in retirement. If you opt for an immediate annuity you begin to receive payments soon after you make your initial investment. For example, you might consider purchasing an immediate annuity as you approach retirement age. The deferred annuity accumulates money while the immediate annuity pays out. Deferred annuities can also be converted into immediate annuities when the owner wants to start collecting payments. Within these two categories, annuities can also be either fixed or variable depending on whether the payout is a fixed sum, tied to the performance of the overall market or group of investments, or a combination of the two.

The Advantages of Annuities

Compounding Interest: An annuity compounds money over time, the earlier you start one, the more money you can receive from it later on.

Minimum Risk: A key advantage to buying an annuity is that the account compounds without being vulnerable to market fluctuations because the insurance company takes the hit.

Invest faster and Defer Taxes: The biggest advantage annuities offer is that they allow you to store away a larger amount of cash and defer paying taxes. Unlike other tax-deferred retirement accounts such as 401(k) s and IRAs, there is no annual contribution limit for an annuity. That allows you to put away more money for retirement, and is particularly useful for those that are closest to retirement age and need to catch up. All the money you invest compounds year after year without being taxed. That ability to keep every dollar invested working for you can be a big advantage over taxable investments.

Endless Income: When you cash out, you can choose to take a lump-sum payment from your annuity, but many retirees prefer to set up guaranteed payments for a specific length of time or the rest of your life, providing a steady stream of income.

The annuity serves as a complement to other retirement income sources, such as Social Security and pension plans.

Disadvantages of Annuities

Before setting up an annuity, there are a few things to take in consideration.

Commissions: For starters, most annuities are sold by insurance brokers or other sales people who collect a commission for bringing your business to the insurance agency. This is normally a one time payment given by the insurance company paid for from a portion of your premium. Some investment companies sell annuities without charging a sales commission or a surrender charge. These are called direct-sold annuities, because unlike an annuity sold by a traditional insurance company, there is no insurance agent involved. With the agent out of the picture there is no need to charge a commission. Firms that sell low-cost annuities include Fidelity, Vanguard, Schwab, T. Rowe Price, Ameritas Life and TIAA-CREF.

Surrender charges: You're also likely to face a prohibitive surrender charge for pulling money out of an annuity within the first several years after you buy it. The surrender charge typically runs about 7% of your account value if you leave after one year, and the fee generally declines by one percentage point a year until it gets to zero after year seven or eight. Note that some annuities come with even heftier surrender charges - up to 20% in the first year depending on the company and product. Also, as with a 401(k) or IRA, in an annuity it's generally not a good idea to take out any money until you reach age 59 ½ because withdrawals made prior to that are hit with a 10% early withdrawal penalty.

High annual fees: If you invest in a variable annuity you'll also encounter high annual expenses. You will have an annual insurance charge that can run 1.25% or more; annual investment management fees, which range anywhere from 0.5% to more than 2%; and fees for various insurance riders, which can add another 0.6% or more. Add them up, and you could be paying 2% to 3% a year, if not more. That could take a huge bite out of your retirement nest egg, and in some cases even cancel out some of the benefits of an annuity. Compare that to a regular mutual fund that charges an average of 1.5% a year, or index funds that charge less than 0.50% a year. But remember, the insurance company is the one taking the risk when investing your money while guaranteeing your money is protected. A key advantage to buying an annuity is the opportunity to realize tax-deferred compounding growth over a long period of time without the risk that comes with investments that are vulnerable to market fluctuations.

Overall, annuities offer numerous options when considering how to prepare for retirement.

For a FREE consultation, Call

Harry Anand

AIM Inc

CA Lic. #0792051.

(909) 985-3659